A peek into Lululemon's financials - Part 2

A peek into Lululemon's financials - Part 2

Learnings from the recently released FY23 10-K Report

In last week’s post, I reviewed Lululemon’s FY22 10-K report to help myself get a base understanding of where Lululemon was as a company a year ago, to help contextualize any growth, changes, or challenges that would be discussed in the earnings press release that was recently released on Thursday, March 21 (available on Lululemon’s investor relations page).

Today’s deep dive will focus on the FY23 10-K report. To prevent repeating myself, if an item hasn’t materially changed between the two posts, I won’t bother mentioning it again.

Before we get into it, I need to provide a little disclaimer:

The Information in this article is my personal opinion and is provided for education, informational and discussion purposes only, without any express or implied warranty of any kind, including warranties of accuracy, completeness, or fitness for any particular purpose. This blog is not intended to be and does not constitute financial advice, investment advice, trading advice or any other advice. You should not make any financial decisions, investments, trades, or otherwise, based on any of the information presented in this article without undertaking independent due diligence and consultation with a professional broker or competent financial advisor. You understand that you are using any and all Information available in this article at your own risk.

A Quick Note on Share Price:

The market did not respond well to Lulu’s FY23 earnings release, with share price dropping over $60 between close of business on Mar 21 to market opening on Mar 22.

Key Takeaways from the 10-K:

Alright, let’s get into it! In no particular order:

Mission, Vision, and Purpose Statement (Page 3):

The mission, vision, and purpose statement is still the same as it was in FY22, with the same language on “connection and inclusion”, despite some of the negative press received last year.

Revenue Segment (Page 4-8):

64% of 2023 net revenue came from women’s range compared to 65% in 2022

79% of 2023 net revenue came from North America geography compared to 84% in 2022

Lululemon shifted reporting its revenue segments from method of purchase (d2c, in store) to regional segments.

Lululemon opened several stores in 2023, operating 711 stores as of January 28 2024, compared to 655 stores on January 29, 2023. Largest increase in stores came from the United States, Canada, and China.

Competition and Differentiation (Page 8-9):

“Competition in the athletic apparel industry is based principally on brand image and recognition as well as product quality, innovation, style, distribution, and price.”

Still a big focus on brand image.

We are in direct competition with wholesalers and direct sellers of athletic apparel and footwear, such as Nike, Inc., adidas AG, PUMA, Under Armour, Inc, and Columbia Sportswear Company. We also compete with retailers who have expanded to include women's athletic apparel including The Gap, Inc. (including the Athleta brand), Victoria's Secret with its sport and lounge offering, and Urban Outfitters, Inc.

No major change in its competitor list either…is Lululemon leadership even in touch with its own competitive market?

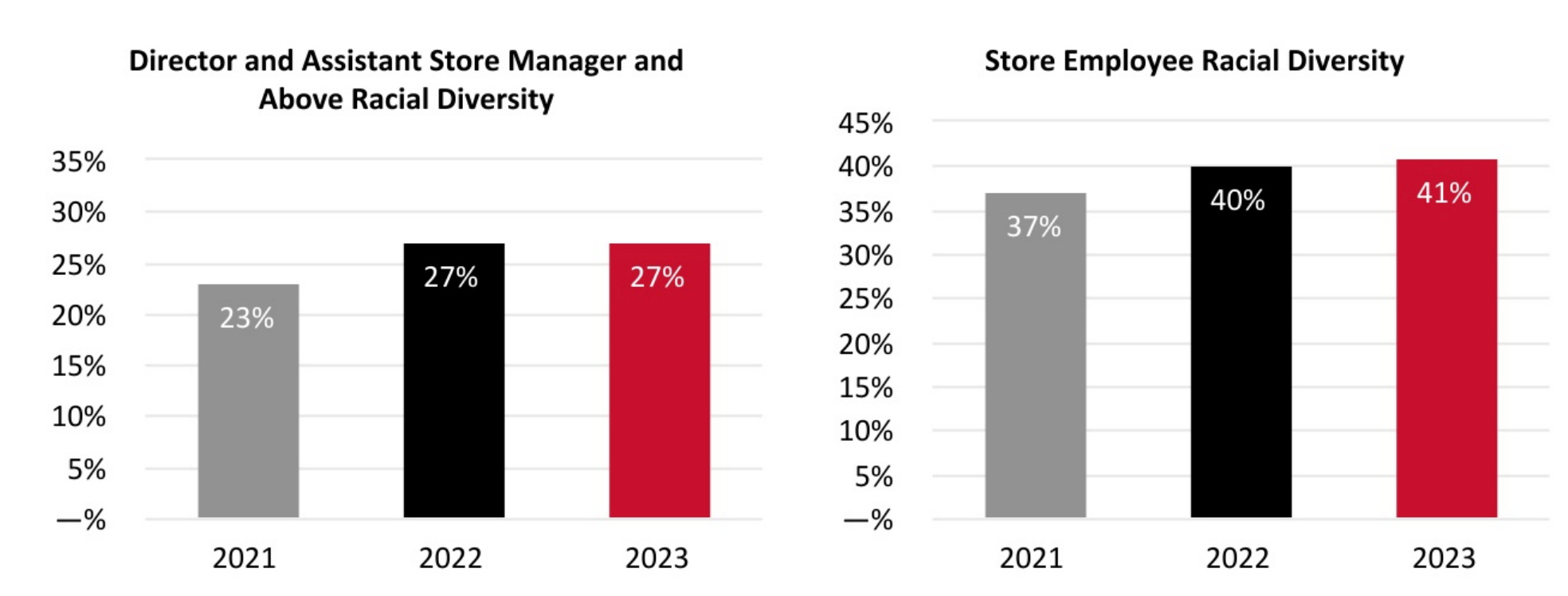

Diversity (Page 8):

No major changes in how they reported diversity metrics, which was a bummer.

Risk Factors (Page 12-24):

No major changes in reported risk factors.

Growth Plans (Page 29):

No additional benchmarks provided for the “Power of Three ×2” growth plans.

Product Innovation (Page 30):

“By innovating through our Science of Feel approach, we continue to seek to solve the unmet needs of our guests. While continuing to see strength from our key collections including Align, Scuba, Define, and Softstreme for women and our ABC collection for men, we launched new innovations as well. For women, we launched Wundermost, our new bodywear collection, we expanded our dual gender golf and tennis assortments. On the men’s side, we launched Steady State and Soft Jersey, to expand our lounge offering, while also enhancing our Pace Breaker short. In accessories, we continued to see strength across our bag assortment, and in footwear we updated our Blissfeel and Chargefeel styles, and in early 2024, we launched our first footwear styles for men. We also announced a new textile-to-textile recycling partnership with the goal of enabling circularity in our supply chain by transforming apparel waste into high quality nylon and polyester.”

There were slight tweaks to the product innovation paragraph in this earnings report and the introduction of the “Science of Feel” innovation approach. Notice the expansion into lounge, golf, and tennis offerings - by widening their product offering, Lululemon is increasing the amount that a consumer would purchase at their store, but the question is - are people interested in the diversified offering?

Lululemon Studio (aka MIRROR) and Membership (Page 66):

“During 2022, the Company decided to shift its lululemon Studio strategy to focus on providing digital app-based services. The Company continued to sell the lululemon Studio Mirror hardware in 2023, and reached the decision to cease selling it during the third quarter of 2023. It also contracted with Peloton Interactive, Inc. to be the exclusive digital fitness content provider to existing lululemon Studio subscribers, and stopped producing its own digital fitness content. The Company ceased selling the lululemon Studio Mirror and new digital content subscriptions in December 2023.” (Page 66)

Lululemon announced the closure of lululemon Studio Mirror.

Financials (Page 29-51):

Net revenue increased $1.5 billion, or 19%, to $9.6 billion in 2023 from $8.1 billion in 2022. (Page 32)

Gross margin percentage increased slightly from 55.4% to 58.3. (Page 32)

Net income increased from $855M in 2022 to $1.5B in 2023. (Page 35)

Final Impressions

Honestly, I was a little bored reading through this 10-K. There weren’t any significant changes in Lululemon’s business model and they didn’t address things like the layoffs or competitor list, like I hoped they would. Lululemon is doing pretty well financially, improving margin and net income and adding about $1 billion of cash on their balance sheet, but I don’t see Lulu doing things to fundamentally improve the quality of the clothes they are selling…they are just selling their clothes in more regions.

Would love to hear from you all - did you learn something that surprised you? Or was there something else you noticed in the 10-K that you’d like to share?

Catch you next Sunday,

Cost per Fit 💰

Interesting to see that their list of competitors seems .. incomplete? While they may be smaller brands, Set Active, Alo Yoga aren’t in there. Neither is dupe culture as a risk factor?

I used to be a yoga teacher so I lived in a lot of workout gear. I could never get myself to purchase from Lululemon even though everyone else had them on (both teachers and students). Something about the brand never spoke to me and I could never find anything that actually fit my body type so never got the hype. Looking into their 10-K somehow makes them even less appealing and I’m happy to have closet free of their products - fully recognizing I’m in the minority.