A peek into Lululemon's financials

A peek into Lululemon's financials

What I learned from reading the FY2022 10-K Report

Lululemon has seen slower growth in recent years, and I believe that is because it is losing connection to the consumer group that launched it in the first place: the matcha girlies. In this essay I explain what led me to that theory, and what Lulu is doing wrong.

In this article, LSD covers the recently declining share price, a scattered product portfolio and brand messaging that may not be connecting with consumers, and some of the negative press the company has received over the years due to comments made by its CEO and allegations of racism at its store locations. I encourage you all to click on that article and read her perspective directly!

Lululemon should be sharing its FY-2023 earnings press release in a couple of days on Thursday, March 21. To prepare for that call, and to help set a baseline level of understanding of the company’s position, I thought I’d read the previous years press release (FY-2022 10-K) which is available on Lululemon’s investor relations page and share my notes with y’all. The idea is that by understanding where Lululemon was a year ago, we can be more informed when trying to answer questions like: Did Lululemon improve? Does Lululemon still face the same challenges or different ones? Are there any key changes to the business model?

Before we get into it, I need to provide a little disclaimer:

The Information in this article is my personal opinion and is provided for education, informational and discussion purposes only, without any express or implied warranty of any kind, including warranties of accuracy, completeness, or fitness for any particular purpose. This blog is not intended to be and does not constitute financial advice, investment advice, trading advice or any other advice. You should not make any financial decisions, investments, trades, or otherwise, based on any of the information presented in this article without undertaking independent due diligence and consultation with a professional broker or competent financial advisor. You understand that you are using any and all Information available in this article at your own risk.

A Quick Note on Share Price:

In LSD’s article, she mentioned that Lululemon’s share price has been declining recently and she’s right. However, I think it’s important to put the share price in perspective - when you look at Lulu’s share price over time, the current share price is actually at the highest levels it has been in the history of Lulu being a public company! It will be interesting to see how the market reacts to the earnings press release info later this week - will share price increase or decrease?

Key Takeaways from the 10-K:

Alright, let’s get into it! In no particular order:

Mission, Vision, and Purpose Statement (Page 3):

“lululemon athletica inc. is principally a designer, distributor, and retailer of technical athletic apparel, footwear, and accessories. We have a vision to create transformative products and experiences that build meaningful connections, unlocking greater possibility and wellbeing for all. Since our inception, we have fostered a distinctive corporate culture; we promote a set of core values in our business which include taking personal responsibility, acting with courage, valuing connection and inclusion, and choosing to have fun. These core values attract passionate and motivated employees who are driven to achieve personal and professional goals, and share our purpose "to elevate human potential by helping people feel their best."

I love reading the first paragraph of 10-Ks because it helps me understand how the company’s leadership views their mission, vision, and purpose. For example, we may just think of Lululemon as an athletic wear company, but Lululemon feels that it’s their purpose to help “people feel their best”. I generally don’t like copying giant bodies of text, but felt it was important in this case as Lululemon has specifically called out its corporate culture in this paragraph, along with the words “connection and inclusion”. Others have mentioned the negative press that Lululemon has received in this Business of Fashion article due to that very topic, and I wonder if the mission, vision, and purpose statement will be tweaked at all in the new earnings release.

Customers are Guests (Page 4):

“Through our vertical retail strategy and direct connection with our customers, whom we refer to as guests, we are able to collect feedback and incorporate unique performance and fashion needs into our design process.”

Lululemon refers to its customers as guests and I thought this was interesting as “guest” is defined by Merriam-Webster as “a person to whom hospitality is extended”. Lululemon is trying to present a luxury and hospitality all the way down to how it names its customers in its earnings release, which has the risk of feeling insincere if the actual experience differs from this portrayal.

Target Market (Page 4):

“Since consumer purchase decisions are driven by both an actual need for functional products and a desire to live a particular lifestyle, we believe the credibility of our brand and the authentic community experiences we offer expand our potential market beyond just athletes to those who pursue an active, mindful, and balanced life.”

Target customers are anyone who wants to pursue an “active, mindful, and balanced life”…which would be most people? What isn’t said here is that their price point prevents the average consumer from accessing their products, so technically their target customers would be anyone who wants to pursue an “active, mindful, and balanced life”…and has disposable income.

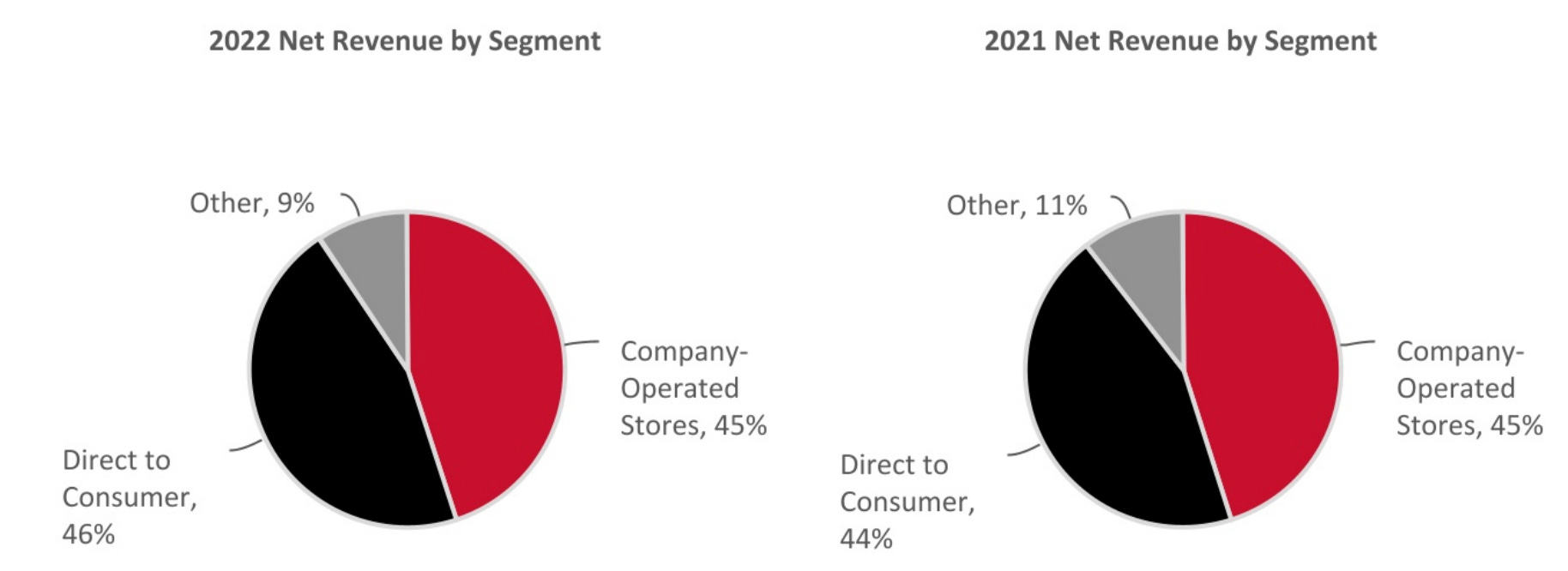

Revenue Segment (Page 4-5):

65% of 2022 net revenue came from women’s range

84% of 2022 net revenue came from North America geography

‘Company Operated Stores’ made up 45% of 2022 net revenue, which was surprisingly high to me - I love shopping online and have only been in a Lululemon store a handful of times to return something or to try on a specific style, but clearly there is a large segment of the population that still loves that in person experience - why do you think that is?

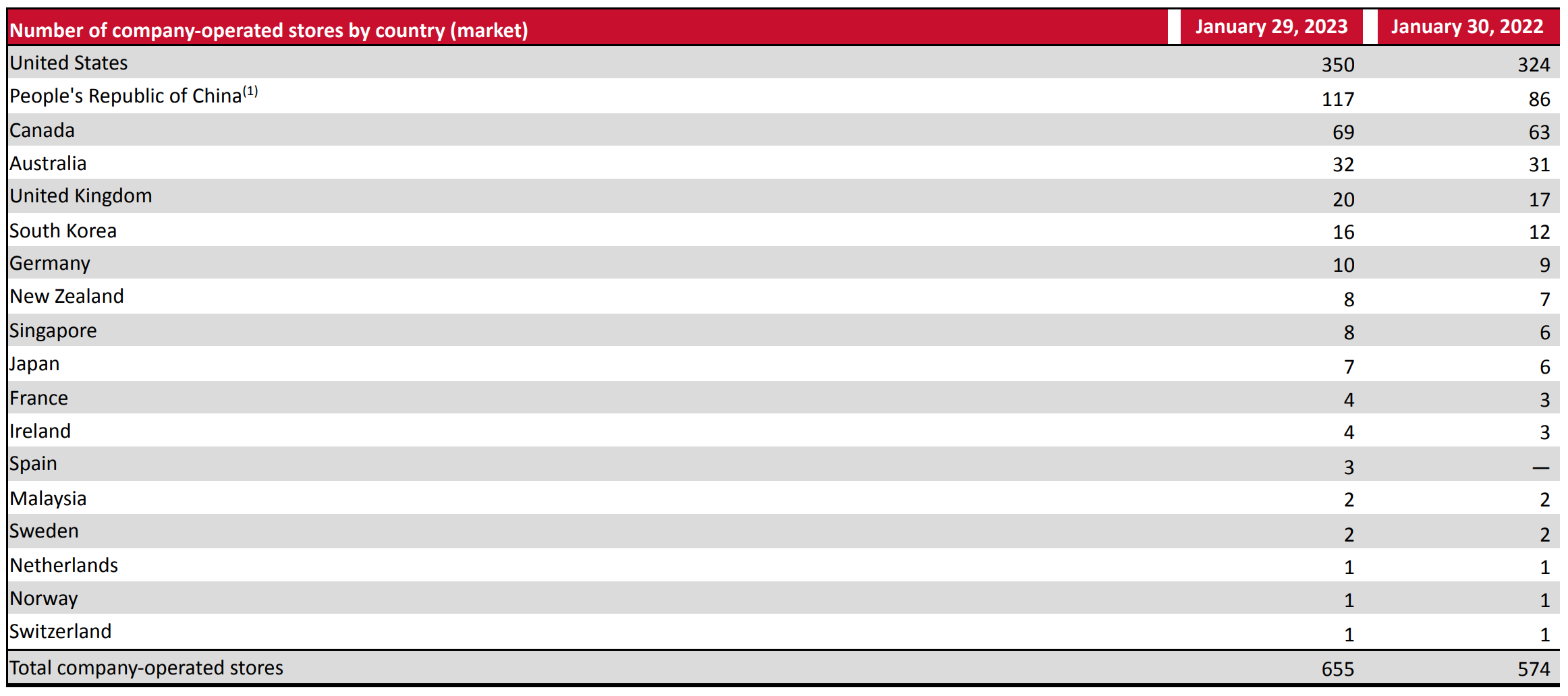

Lululemon operated 655 stores on January 29, 2023, with the United States unsurprisingly having the most stores at 350. What was surprising to me was that the People’s Republic of China had the second highest stores at 117. I’ll be curious to see if this changes in the next earnings release.

Sourcing and Manufacturing (Page 7):

Lululemon does not own or operate any manufacturing or supplier facilities and does not have any long-term contracts with a majority of them, which means they have to compete with other companies for fabrics, raw materials, and production. In my opinion, manufacturing and supplier vendors are well diversified in location (see below).

Lululemon works with 45 vendors to manufacture products; “During 2022, 39% of our products were manufactured in Vietnam, 14% in Cambodia, 12% in Sri Lanka, 8% in Bangladesh, and 7% in Indonesia, and the remainder in other regions.”

Lululemon works with 60 suppliers to provide the fabrics for products; “During 2022, 43% of our fabrics originated from Taiwan, 19% from China Mainland, 16% from Sri Lanka, and the remainder from other regions.”

Competition and Differentiation (Page 7):

“Competition in the athletic apparel industry is based principally on brand image and recognition as well as product quality, innovation, style, distribution, and price.”

I thought it was so interesting that Lululemon thinks that competition in the athletic apparel industry is based principally on brand image and recognition. This means that to them, the most important differentiating quality (and what they will pay most attention to) is their brand image. In contrast, imagine if an athletic apparel company were say that the differentiating quality is product quality above all else - would that make you think differently about the company and its products compared to a company that says that brand image is the most important?

We are in direct competition with wholesalers and direct sellers of athletic apparel and footwear, such as Nike, Inc., adidas AG, PUMA, Under Armour, Inc, and Columbia Sportswear Company. We also compete with retailers who have expanded to include women's athletic apparel including The Gap, Inc. (including the Athleta brand), Victoria's Secret with its sport and lounge offering, and Urban Outfitters, Inc.

I thought it was interesting that no other D2C companies like Vuori, Gymshark, Girlfriend Collective, or Athleta were on the list. I wonder if that will change for the upcoming earnings release.

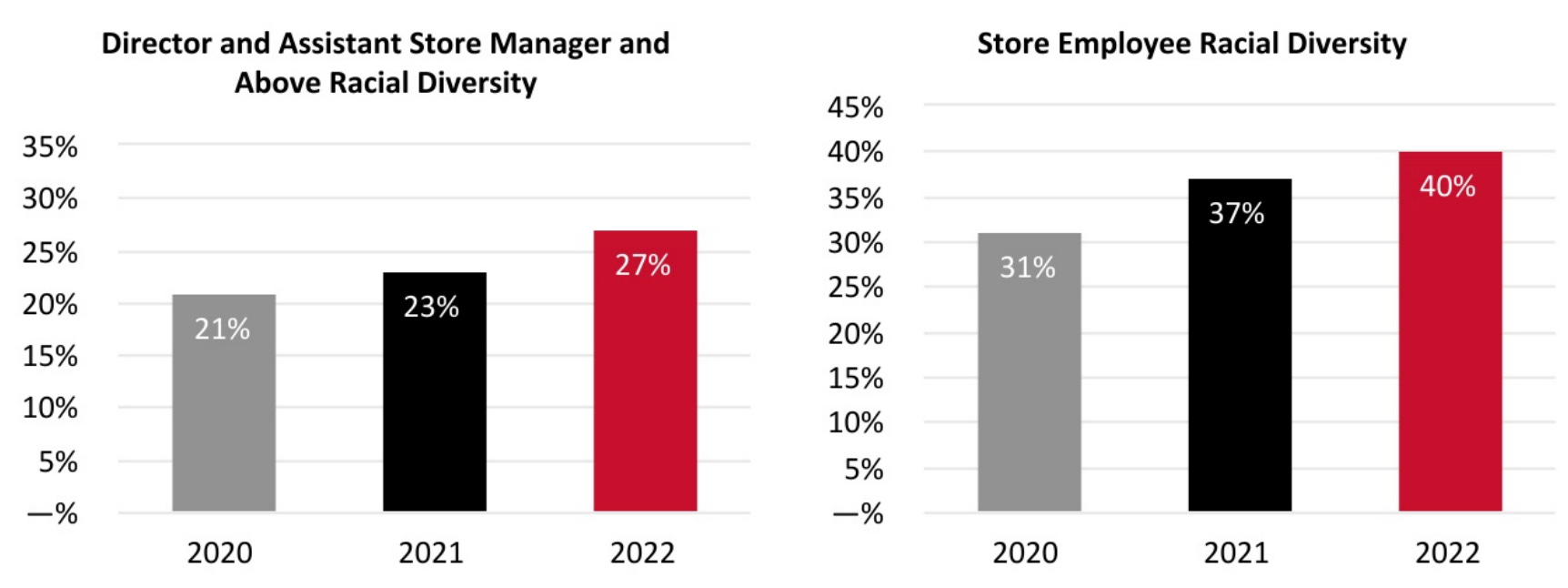

Diversity (Page 8):

Lululemon has a whole section in their FY-2022 10-K on diversity and their goal of “advancing a culture of Inclusion, Diversity, Equity, and Action (“IDEA”)”. I love that they are reporting on this, but I’d love a little bit more detail. For example, they’ve included this chart that reports “Store Employee Racial Diversity” across North America, Europe, Australia, and New Zealand, but a footnote at the bottom explains that “"Racial diversity" is used to measure the non-white population.” I’ll bring up the Business of Fashion article from earlier and ask - what percentage of its employees are black? I wonder if they will provide any additional information on this in the next release.

Risk Factors (Page 8-20):

This section outlines risks to the business which could materially impact the company. Nothing really stood out to me here - it was mostly straightforward and reasonable. The first risk in this section was, “Our success depends on our ability to maintain the value and reputation of our brand.” They are really going all in on this brand thing…

Growth Plans (Page 26-27):

In 2022, management announced its new 5 year growth plan, “Power of Three ×2”. The benchmarks are not clearly defined in the 10-K (in fact, this management note is the only place that this term is even mentioned), but are focused on areas like product innovation, guest experience, market expansion, revenue growth in mens, d2c, international, and core business. This all sounds pretty generic to me, so I’m curious if we’ll get to see more benchmarking in the next earnings release.

Product Innovation (Page 26):

We continue to solve for the unmet needs of our guest by bringing new technical innovations into our merchandise assortment. In 2022, we expanded our core running category with the launch of Senseknit, a proprietary fabric technology offering zoned compression. We entered new activities with our capsule collections for golf, tennis, and hiking. And we launched footwear, enabling us to provide a head-to-toe solution to our guests. The footwear collection currently includes three technical styles – Blissfeel, Chargefeel, and Strongfeel – all designed specifically for women. In addition, we launched a dual gender slide for pre- and post-workouts.

I copied this whole paragraph, because that’s all that Lululemon had to say about its product innovation…that one little paragraph. Obviously, Lululemon won’t want to give away any proprietary info, but surely they could have explained a little bit more their process, some guest feedback metrics, or even quantified technical improvements in some of these newer innovations. Lululemon has already told us that their most important differentiator (in their perspective) is their “brand image”, but I was still a little surprised at how light this section was.

Lululemon Studio (aka MIRROR) and Membership - varies, see below:

Lululemon announced its intention to acquire MIRROR in 2020 for a purchase price of $500M, subsequently re-branded [it to] "lululemon Studio," and $362.5 million of goodwill was allocated to the lululemon Studio reporting unit. (Page 39)

As explained in this Investopedia article, Goodwill refers to the “portion of the purchase price that is higher than the sum of the net fair value of all of the assets purchased in the acquisition and the liabilities assumed in the process”. Meaning, at the time of purchase, Lululemon believed that $362.5M of the value in MIRROR was due to intangibles like “the value of a company’s name, brand reputation, loyal customer base, solid customer service, good employee relations, and proprietary technology”. (Investopedia Article)

Well, in the FY-2022 report, Lululemon indicated that it was not able to meet its subscriber or revenue goals for lululemon Studio which indicated the need for an impairment test which “led to the recognition of an impairment of goodwill of $362.5 million.” (Page 39) For reference, this Investopedia article about goodwill impairment explains that “Goodwill impairment arises when there is deterioration in the capabilities of acquired assets to generate cash flows, and the fair value of the goodwill dips below its book value.” Essentially, the fair value of those “intangibles” that Lululemon had paid for were not worth the original estimated value (and book value).

The tldr is that Lululemon made a bad investment in MIRROR, in retrospect. I added “in retrospect”, because in heights of the covid pandemic in 2020, virtual home workout hardware probably sounded like a really good investment. I think they had right idea with the investment into a membership type home workout tool, but executed it poorly…they didn’t need to buy a whole company to get into home workouts, they could have just done it. Well, a new two-tier membership program was announced in October 2022 and check out the third bullet (Page 27):

The first tier (Essential membership tier) is free and “provides access to select content, as well as certain benefits in-store and online”.

lululemon Studio is the “premium paid tier of the program which offers members a connected fitness experience via in-home hardware”

Lululemon plans to expand “the lululemon Studio premium tier by enabling guests to access digital fitness content via a new app, launching in summer 2023, for a lower monthly fee”

We’ll see that this digital fitness content is pretty short lived as Lululemon will announce a partnership with Peloton in September of 2023, in which it states it will, “discontinue selling the lululemon Studio Mirror before the end of the year and will continue to provide ongoing service and support for Mirror devices” and will also “discontinue its digital app-only membership tier on November 1, 2023”. I’m sure we’ll read all about this in the next earnings release!

Inventory (Page 26):

In 2021 and 2022 we experienced supply chain disruption, including delays in inbound delivery of our products as well as in manufacturing. This supply chain disruption caused us to use higher cost modes of transport, including increasing our use of air freight. The supply chain disruption we have experienced has contributed to the 50% increase in our inventory balance as of January 29, 2023 compared to January 30, 2022.

I’ve been personally a little frustrated due to the lack of inventory or sizing or colors available on Lululemon in the past year or so, and it’s interesting that this was flagged as a known challenge due to supply chain disruption. It’s been about a year since this report was released, so I’m curious to see if this issue will persist in the next earnings release.

Financials (Page 29-51):

Net revenue increased $1.9 billion, or 30%, to $8.1 billion in 2022 from $6.3 billion in 2021. (Page 29)

Gross margin percentage decreased slightly from 57.7% to 55.4%. (Page 30)

Net income decreased from $975M in 2021 to $855M in 2022. (Page 33)

What will I be looking for in the next earnings release?

Here are a few areas that I hope the next earnings release will address:

Is Lululemon still profitable? What are the trends in revenue, gross margin, and net income?

Is the “Power of Three ×2” growth plan still the same? Have better benchmarks been provided?

Has the mission, vision, or purpose statement been updated?

Are revenue segments similar to what they were in FY-2022?

Is the supplier and manufacturer strategy similar to what it was in FY-2022?

Is “brand image” still the key differentiator?

Has Lululemon recognized competitors like Vuori and others?

How does Lululemon talk about diversity? Has more detail been provided on the percentage of employees that are black?

What happened with lululemon Studio and the subsequent partnership with Peloton? Has this proved to be a better financial investment?

Are there any new risk factors that have been mentioned?

Lululemon announced a couple of rounds of layoffs last year - how is that addressed in the 10-K?

What is up with inventory?

Would love to hear from you all - did you learn something that surprised you? Or was there something else you noticed in the 10-K that you’d like to share?

Catch you next Sunday,

Cost per Fit 💰

love this! the substack community really is amazing, look forward to what conclusions you will draw after their FY23 reports come out, if you are planning to address it in a separate post. I specialise in supply chain as a management consultant; retailers were def hit hard by covid and other ensuing disruptions, some companies have been really clever and quick in their responses - let's see what Lululemon's was.

I still love my Lulu aligns but agree with LSD that they have just not been keeping up their brand or staying current. I think that shows in the companies that they indicate are their competitors… I assume that will change this year but to mention Victoria’s Secret vs. the other more current brands seems way off.

I am primarily an online shopper too but I do end up going into the store to try athletic wear when I can as I find the fit can be so different from item to item.

Thanks for this analysis! Would love your thoughts on Outdoor Voices!